Collapse almost never looks like collapse when you’re living through it.

It looks like a steady paycheck and only small, forgettable changes in the prices of everyday things. It looks like a forest where every small blaze is put out as soon as it appears and the air always smells clean. It looks like a pension statement projecting a comfortable monthly income in retirement, a central bank promising “stability,” and a balanced city budget thanks to one more quiet line of borrowing. Nothing on any single page feels catastrophic.

Only later, when the currency fails, the forest burns beyond control, or the pension admits it cannot pay obligations, does the pattern become obvious. For years, small stresses were being smoothed away. Volatility was managed, pain deferred, risk hidden. What felt like protection at the level of the individual was, in reality, accelerating the decay of the entire system—and when the system finally breaks, it takes those same individuals it was meant to protect down with it.

At first glance, it seems as if everything comes down to ideology: capitalism against socialism, big government against small, stricter rules against freer markets. We treat those ideological battles as if picking the right side will save us, but we keep repeating the same deeper mistake. Again and again, we humans tend to replace messy, decentralized trial-and-error with engineered “stability,” turning living ecosystems into machines that look efficient on the surface while quietly corroding their own foundations over time.

If we want something better, we need a different way of seeing the universe itself. In the essay that follows, I’ll borrow tools from physics (friction and entropy), information theory (signal versus noise), and universal Darwinism (variation, selection, retention) and apply them to not just economics and finance, but to everything. The goal is not a utopian blueprint, but a quieter and more durable idea: how can we design systems that constantly renew their parts and keep failure frequent, truthful, and small, rather than rare, hidden, and catastrophic?

The Problem

Work, Reward, and the Inevitability of Economic Friction

To understand how physics, information theory, and universal Darwinism manifest in the everyday lives of individuals, let’s start with the relationship between employers and employees.

Employees expend energy through their labor to advance their employer’s objectives. In return, they receive a paycheck which represents a ratio of energy expended to monetary reward, which we’ll call the work-to-pay ratio (W2P ratio).

Now, let’s introduce the concept of ‘friction’ within this system. In physics, friction is the force that opposes motion, transforming kinetic energy into other and often less useful forms. In our analogy, friction manifests as taxes, inflation, and more. These elements act as a ‘drag’ on your W2P ratio, akin to how aerodynamic drag reduces the efficiency of an airplane.

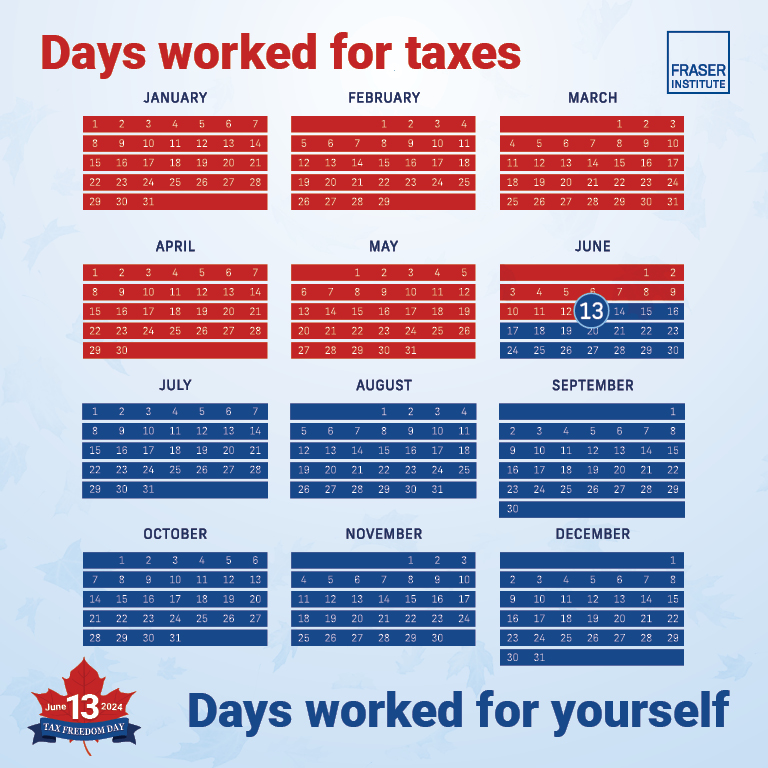

As an example, consider the median household income of approximately $78,438 in Charlotte, NC. After federal and state taxes, the after-tax income is about $64,380, representing a loss of $14,057 to taxes alone, which is equivalent to 2.15 months or 372.4 hours of work.

But taxes aren’t the only source of friction. Inflation further erodes purchasing power, especially when it outpaces salary increases. Suppose the average salary increase is 3% per year, but the inflation rate is 5% per year. This means employees effectively lose 2% of their real income annually because their wages aren’t keeping up with the rising cost of living. During the 2023–2024 period, if we assume an all-in effective tax rate of roughly 25% and a 2% loss of real income to inflation then American workers effectively “lose” about 3 months of work to taxes and roughly another week to inflation—around 3.2 months of their labor’s value each year.

Additionally, Argentina has been experiencing extreme inflation—reaching rates over 117.8% in recent years. Which means that, on average, the cost of living has more than doubled in single year. If wages remain stagnant, the purchasing power of a worker’s income falls to only about 45.9% of what it was before. In other words, the worker effectively loses about 54.1% of the purchasing power they would have needed to maintain the same standard of living. Interpreted on a monthly basis, this loss is equivalent to about 6.49 months (0.541 × 12 months) of income lost to inflation. Combined with the months lost to taxes, workers in Argentina are effectively losing about 9.49 months of work annually due to taxes and inflation.

If Canadians paid all their taxes up front, they would work the first 164 days of this year before bringing any money home for themselves and their families.

June 13, 2024. www.fraserinstitute.org

Conversely, employers (or the owners of the companies) often have a work-to-pay ratio that exceeds the direct value of their individual labor (a W2P ratio above 1.0). Similar to a regenerative braking system, which converts the friction from braking into usable electrical energy for a car, employers benefit from the collective labor of their employees, partially converting the “friction” experienced by employees into financial gains for themselves.

Although this dynamic may seem imbalanced, it is a natural outcome inherent in complex systems. Just as physical friction is essential for many fundamental processes—enabling us to walk without slipping, allowing vehicles to stop, and facilitating the generation of heat and energy—economic friction also serves a vital purpose.

Without the prospect of riches and/or fame, many business owners wouldn’t have deemed the risk of entrepreneurship worthwhile. Companies must generate profits as it provides the incentive for their existence. Countries must levy taxes on their citizens to prevent invasion and the collapse of public utilities. However, the very thing (friction) that’s needed to enable the survivability of a system is the same thing which guarantees its destruction.

Entropy

According to the second law of thermodynamics, the level of entropy (which is a scientific way to describe chaos, uncertainty, or decay) can only increase within a system over time; it can never decrease. Only a perfectly efficient system with no friction (or loss of energy) can avoid the inescapable rise in entropy and the eventual death of that system. But, as if by cosmic decree, not one system within our three-dimensional reality lies beyond the influence of entropy – a fact that underscores the transient nature of all things – nothing and no one will survive the test of time.

This inevitable fate is caused by a relentless mechanism: friction. By driving an irreversible dissipation of energy, friction fuels a system’s entropy. It acts not merely as a byproduct of motion but as the catalyst of decay, constantly bleeding the system of its vitality until it inevitably fails.

It is a fundamental truth that friction is the force that ignites motion and fuels progress, yet it is also the agent of entropy that gradually leads everything to decay.

While economic friction is essential, driving the very processes that keep our economic engine running, its balance is delicate. Excessive friction, be it through over-taxation, ever increasing income disparity, or inflation, will lead to negative outcomes like tax evasion, job dissatisfaction, and a general disregard for laws or rules. Understanding and managing these economic frictions is crucial for sustaining a productive and equitable economic system.

The Economic Effects of Economic Frictions

While traditional indicators such as the Gini coefficient, which measures income inequality, and the Human Development Index (HDI), assessing overall well-being, provide insights into “societal health” and potential unrest, they often fall short in pinpointing the root causes of friction. Behavioral economic tools that gauge public sentiment and other social indicators like crime rates, educational attainment levels, and public health metrics can signal underlying societal stressors, but they too have limitations. In fact, one of the most effective ways to understand these tipping points and the inherent frictions leading up to them is by exploring historical examples. History, with its rich tapestry of economic successes and failures, offers invaluable lessons and patterns that can guide our understanding of current and future challenges.

The Roman Empire: A Case Study in Economic Friction and Entropy

The decline and fall of the Roman Empire, particularly during the 3rd and 4th century AD, serves as a vivid illustration of how economic friction can usher in entropy, leading to societal chaos and the eventual collapse of that society.

Currency Debasement and Rampant Inflation

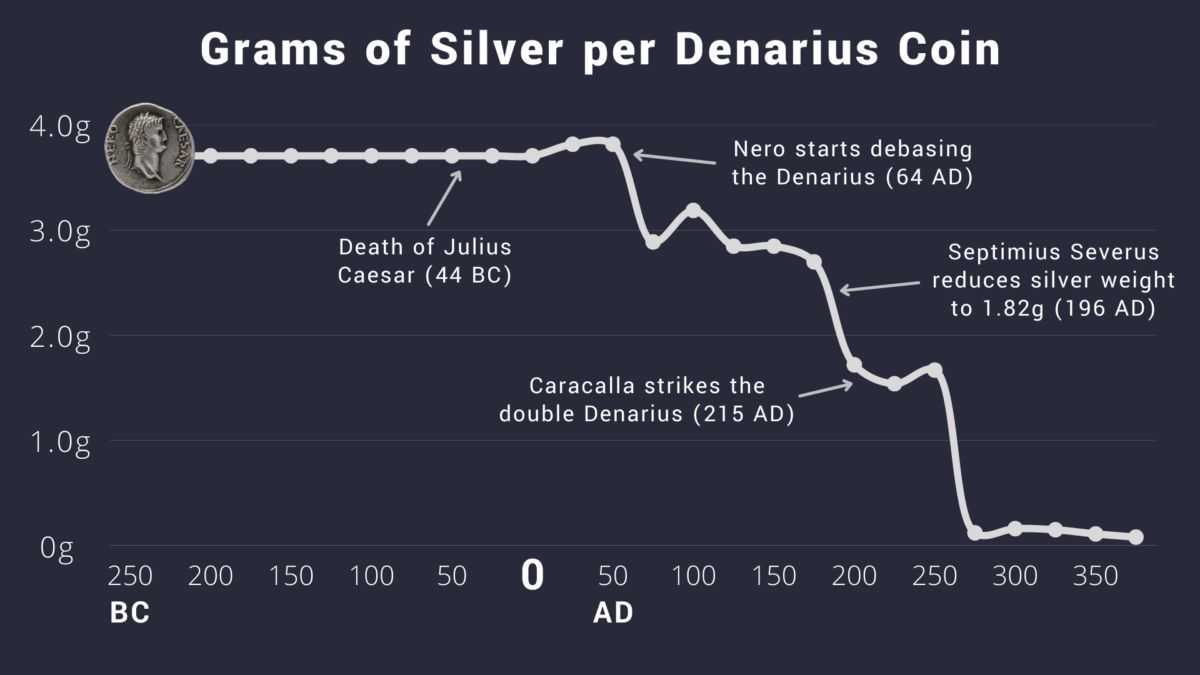

One of the most significant factors contributing to Rome’s decline was rampant inflation caused by the debasement of its currency. The silver content of the denarius, Rome’s primary coin, was systematically reduced over time. Around 211 BC, the denarius was approximately 95% pure silver. By AD 270, its silver content had plummeted to a mere 3-5%.

This drastic reduction undermined the currency’s value and stability. As the intrinsic worth of the denarius diminished, prices for goods and services soared, eroding the purchasing power of wages. Workers found that their earnings bought less and less, effectively reducing their work-to-pay (W2P) ratio. This devaluation introduced significant economic friction:

- Erosion of Savings: Citizens who had saved money found their wealth rapidly losing value.

- Market Instability: Merchants and traders faced uncertainty in pricing (increased entropy), leading to decreased trade and commerce.

- Loss of Confidence: The public’s trust in the currency—and by extension, the government—waned.

The uncertainty and instability surrounding the denarius led to increased entropy (chaos) within the economy. With money losing its reliability as a medium of exchange and store of value, economic transactions became more chaotic and less efficient.

Excessive Taxation

Inflation wasn’t Rome’s only economic woe. In certain provinces, tax rates escalated to an alarming 33% of agricultural produce. Importantly, this was a tax on gross output, not net income, meaning farmers owed a third of their total harvest regardless of their expenses or losses.

To illustrate the severity, consider a modern analogy: In 2022, Apple Inc. paid $19.3 billion in income taxes on its profits. If Apple were taxed at 33% of its total revenue (approximately $316 billion), its tax bill would have surged to over $104 billion. Such a burden would be a death warrant, even for a global mega corporation.

This high taxation left many farmers reliant on their next harvest. The crops they managed to harvest were immediately sold to cover the cost of taxes. If barbarians, a drought, or locusts destroyed their crops, they borrowed from neighbors, starved, or were jailed by the State. Some Romans even resorted to selling their children or became a “nexus” (a debt slave) to settle debts.

By the latter part of the third century the currency was so worthless that the State resorted to forced labor… the State was so unable to rely on money to meet its needs that it collected its taxes in the form of supplies directly usable by the military and other branches of government, or in bullion to avoid having to accept its own worthless coins.

Joseph Tainter, The Collapse of Complex Societies

Such burdensome taxation introduced a level of economic friction that many found intolerable – incentivizing rampant tax evasion. When citizens perceive taxes as overly oppressive or unjust, they naturally seek ways to safeguard their earnings, even if it means skirting the law.

Corruption and the Breakdown of Institutional Trust

Economic hardships were further exacerbated by rampant corruption and a lack of effective legal protections within the Roman Empire. Government officials, tax collectors, and even military personnel frequently exploited their positions for personal gain. Practices such as bribery, embezzlement, and abuse of power became commonplace, severely straining the empire’s economic fabric. When tax revenues were siphoned off for personal use rather than being invested in essential national needs, it introduced significant friction into the economic system. Decaying public infrastructure became a visible sign of this friction, undermining the efficiency and reliability of essential services. Moreover, the misuse of tax proceeds eroded public trust, increasing entropy by diminishing citizens’ expectations of future governmental support and spending.

As institutions failed to uphold justice and equity, social cohesion eroded, fueling friction. Citizens grew increasingly unwilling to obey laws or support communal initiatives, compounding social entropy and rendering Rome a more fragile polity.

The Rise of Black Markets and Informal Economies

Faced with oppressive taxes and a worthless currency, many Romans turned to black markets and barter systems. This shift wasn’t just about evading taxes, it was a survival strategy. Operating outside the formal economy allowed people to protect their wealth by trading goods directly, avoiding the diminishing value of the denarius.

While this may have provided short-term relief for individuals, it further reduced the state’s tax revenue. With less income, the government struggled to fund essential services, maintain infrastructure, or pay the military. This decline in state capacity accelerated the empire’s downward spiral.

This decline in formal economic activities, combined with a rise in crime and lawlessness, further reduced the taxable base. With fewer revenues, the state found it increasingly challenging to maintain public services, defend its borders, and uphold law and order. All these factors and more created a negative feedback loop. The more the economy declined, the more people withdrew from the formal system, further exacerbating the decline.

The fall of the Roman Empire underscores a timeless truth: when economic friction goes unaddressed and entropy rises unchecked, even the mightiest of societies can crumble. By debasing their currency, overtaxing their citizens, allowing corruption to flourish, and failing to maintain public trust, Rome set itself on a path towards inevitable decline. If we learn from Rome, we can work to reduce unnecessary friction and keep things in balance, helping our own systems to be more resilient and to stand the test of time.

Argentina’s Current Economic Challenges: A Modern Reflection of Historical Crises

Once considered among the world’s wealthiest nations, Argentina now contends with severe economic challenges: nearly 53% of its population lives below the poverty line, and inflation has soared to 289.4% in recent estimates. Like Rome, Argentina’s troubles illuminate how friction—when it exceeds the essential “maintenance” level—spurs destructive entropy and can threaten the survival of the entire system.

Inflation in Argentina has become so entrenched that high rates are now an expected norm. The continuous devaluation of the Argentine peso, reminiscent of the Roman denarius’s debasement, has wreaked havoc on savings, pushed investors to take greater risks, and forced citizens to rely on foreign currencies or barter systems. This relentless currency devaluation serves as a significant source of economic friction, reducing the work-to-pay (W2P) ratio and perpetually increasing poverty levels.

Taxation, a fundamental tool for any government, has paradoxically become a double-edged sword in Argentina. Excessive and poorly managed taxes have led to widespread evasion, further destabilizing the economy and escalating entropy. Additionally, Argentina’s persistent struggle with sovereign debt, marked by multiple defaults, has eroded investor confidence.

Corruption and inefficiency have severely tarnished Argentina’s reputation. Mismanagement of public funds and a lack of transparency have eroded public trust, reminiscent of the dwindling faith in Rome’s political system. This erosion fosters social unrest and chaos, adding another layer of economic instability. As trust in institutions declines, citizens are more likely to withdraw from the formal economy, seeking refuge in informal markets.

Argentina’s economic journey is characterized by a series of negative feedback loops. Hyperinflation, debt crises, and public distrust reduce investor confidence, which in turn exacerbates these very challenges. The friction between labor input and monetary reward, amplified by misguided monetary and fiscal policies, propels the society towards less structured and inefficient economic systems. High transaction costs and the inefficiencies of black-market dealings incentivize individuals to seek alternative systems, perpetuating a cycle of systemic collapse that inhibits and rapidly diminishes global economic growth.

Argentina’s predicament is a modern-day portrait of friction outpacing a society’s resilience. By surpassing the basic administrative and fiscal thresholds necessary for stability, these “excess” frictions produce escalating entropy that pushes Argentina to the brink—echoing the cautionary tale of ancient Rome.

Part 1: Conclusion

From the collapse of the Roman Empire to Argentina’s modern economic turmoil, we see that friction—particularly through devalued currencies, heavy taxation, and corruption—can serve as an underlying force of entropy that nudges entire societies toward collapse. However, friction at a reasonable level is also essential; without taxation, no nation can fund the infrastructure and services needed for stability. The true peril emerges when friction surpasses that sustainability threshold—when the burdens on individuals and institutions far exceed what is necessary to keep the system functional.

So, if friction is here to stay, what can we do to push it back? Information. More specifically, truthful information. Honest prices, transparency, clear rules, and plain incentives minimize uncertainty (entropy) at the root. And because higher friction → higher entropy → higher volatility, resolving uncertainty also reduces volatility. Crucially, information works not by piling up more of the same, but by bringing new truth to light—fresh measurements, new participants and perspectives, births and discoveries (a new human in a society, a new star in a cosmos). This novelty refreshes the system’s state space and resets entropy. With lower uncertainty, resources reallocate faster, and course corrections come earlier. Put simply: opacity increases friction which increases entropy—and then volatility; transparency supplies new truth that turns friction into traction, and volatility into learning. Next, we’ll examine information theory to see why protecting signal is the first step towards antifragility.

Information & Volatility

The War Against Entropy

Information is defined as the resolution of uncertainty. When information (more specifically, truth) is at its lowest, that is when entropy (or chaos) is mathematically at its highest. This correlation is deeply rooted in information theory, a branch of mathematics and telecommunications. In this context, ‘information’ is understood not just as data, but as meaningful and reliable data that reduces uncertainty about a particular state or outcome.

When truth is abundant and easily accessible, our environment becomes more ordered and predictable. Conversely, as truth becomes scarce, misinformation and ambiguity proliferate, this results in a state of confusion and chaos.

As an example, a coin-flip has a binary characteristic since it can only result in either heads or tails. The graph displays entropy, denoted as H(x), on the y-axis for a symbol with two possibilities (binary). It is worth noting that entropy, defined as uncertainty within information theory, reaches its maximum value of 1 near the midpoint of the graph. When we toss a coin, the level of uncertainty about which side it will land on is highest at the peak. Conversely, the level of disorder, or entropy, is at its lowest (equal to 0) when we know the current value of the binary symbol at either end of the x-axis.

This inverse relationship between information and entropy can be observed in social systems, communication networks, and even ecological systems. As one example, in Finance we have the Efficient Market Hypothesis (EMH) which is a fundamental concept that suggests financial markets are one of three forms of efficiency (weak, semi-strong, and strong). According to EMH, the more information that is reflected in asset prices, the more efficient the market becomes. In other words, market entropy (chaos) is inversely correlated with the amount of information embedded in prices.

In a free market every transaction reflects the collective’s knowledge, expectations, and sentiment. When new information enters the market - be it a company’s earnings report, changes in economic policy, or geopolitical events – investors reassess the future value of assets discounted to today, leading to price adjustments. But many fail to realize that even a seemingly minor decision—such as whether a mother buys (or doesn’t buy) milk at the grocery store—can influence the price of milk. Prices, therefore, are not merely numbers but encapsulations of all known information at a given moment. They compress nearly unlimited amounts of data into a single data point.

The challenge lies in ensuring the free flow and accuracy of information to minimize entropy and create a more predictable and efficient market. However, we humans have a tendency to unknowingly impair the propagation of such information or truthfulness in the false hopes of lowering volatility.

If we consider prices to be the compression of information into a single data point, then isn’t volatility simply the adjustment of prices towards truth as new information is created and observed? This perspective suggests that volatility is not a risk factor to be minimized or maximized, but a vital process of truth-seeking and course correction within markets.

Volatility Is Not Risk

Humankind inherently strives to mitigate volatility, often viewing this effort as both a pragmatic necessity and an ethical obligation. To this end, we have developed various institutions and practices aimed at cushioning the uncertainties and disruptions inherent in both finance and nature. However, this conventional approach to volatility represents a cognitive oversight in our understanding of its true role.

If information is the resolution of entropy, and volatility is the adjustment of reality to new information, then by dampening volatility, we add friction to a system’s natural method of self-correction. Consequently, this leads to the propagation of entropy within our systems, hastening its eventual destruction. Essentially, we are faced with a trade-off: opting for either painful short-term volatility or fatal long-term volatility.

How Small Fires Turn into Infernos

We can clearly see this tradeoff between painful short-term volatility or fatal long-term volatility in the Yellow Pine and conifer forests that span across both the United States (specifically Alta California) and Mexico (particularly in Northern Baja California). After decades of implementing divergent fire management strategies, there are now stark differences in the health and resilience of these forests.

In the United States, the strategy has revolved around strict management, primarily focusing on the immediate extinguishing of wildfires. This approach aims to dampen short-term volatility, which is represented by frequent, smaller fires. However, this practice has introduced friction and effectively blocked nature’s own mechanism of clearing dead trees and underbrush. Smaller, more frequent fires, which are a natural part of the forest ecosystem, play a crucial role in maintaining its health and balance. The U.S. policy of fire suppression has, paradoxically, facilitated the accumulation of dense underbrush and debris, thereby laying the groundwork for increasingly destructive fires.

On the other hand, Mexico has historically adopted a more laissez-faire approach (whether intentional or not) towards managing its Yellow Pine and conifer forests. This approach allows wildfires to naturally run their course, respecting the natural fire cycle of these ecosystems. As a result, the forests in Northern Baja California tend to have a lower density of underbrush, reducing the fuel for potentially large-scale fires and thus maintaining a more natural ecological balance.

The ramifications of this contrasting approach are profound. In Alta California, the sheer intensity of the larger fires, supercharged by the accumulated underbrush, is terrifying. These supercharged wildfires not only destroy the vegetation but the heat from the fire is so intense that it burns off the topsoil, leaving a scarred and barren landscape in its wake. This destruction goes beyond the immediate loss of trees and wildlife; it undermines the land’s fertility and ecological integrity, leading to long-term consequences such as soil erosion, reduced water retention, and loss of biodiversity.

The annual average area burned in 2020-2023 was 3x higher than in the 2010s.

July 1, 2024. oehha.ca.gov

This scenario underscores a paradox in human intervention: while efforts are made to reduce short-run volatility, such as the immediate threat of small fires, these actions can inadvertently lead to more profound volatility and lasting damage. This challenges the very objectives that interventionist policies seek to accomplish. Instead of enhancing forest resilience and health, such policies can exacerbate vulnerability to catastrophic events, highlighting the need to alter how we currently view volatility.

Pension Funds: A Catalyst for Mass Poverty

Pension systems, arising from a fundamental misunderstanding of volatility, are introducing chaos (entropy) into their environments, with profound implications not only for retirees but also for current workers. By promising smooth, “guaranteed” income in old age, they centralize responsibility for retirement in a handful of fragile institutions and dull the information signal that individuals must build their own resilience.

Historically, many American businesses offered pensions as a guaranteed source of retirement income, leading workers to rely heavily on them. When numerous corporate pensions, particularly in industries like steel and airlines, went insolvent, thousands of workers were left with little to no retirement savings. Companies like Bethlehem Steel and United Airlines left tens of thousands of employees scrambling for financial security when their pension obligations were underfunded; the Pension Benefit Guaranty Corporation (PBGC) stepped in, but many retirees received only a fraction of their promised benefits. The volatility that should have shown up gradually—in market prices, in funding ratios, in individual account balances—was deferred, then arrived suddenly as mass poverty risk.

The on-going pension crisis in Chicago is another prime example. The city’s pension funds are all below the 40% threshold experts have cited as likely doomed to insolvency and over 80% of property taxes are allocated to pension payouts. As a result, Chicago has been forced to make difficult trade-offs, including cutting spending on critical infrastructure, education, and public safety. Each tax hike and service cut adds friction to the local economy and increases entropy in the social system, creating a negative feedback loop that threatens the city’s long-term financial stability.

At the national level, America’s Social Security system functions as a gigantic, government-run pension fund with similar fragilities. In 2024, the federal government spent roughly $1.5 trillion on Social Security (about 21% of all federal spending) with around $1.3 trillion of that going to retirement benefits alone!. These promises are not primarily backed by accumulated savings, but by ongoing payroll taxes: workers and employers together surrender 12.4% of every paycheck (up to a cap) to keep the system afloat. As demographics shift and the worker-to-retiree ratio falls, the system runs an ever-increasing deficit which requires the selling of trust-fund assets and the issuing more federal debt. In information-theoretic terms, Social Security keeps most people’s true retirement position opaque: the illusion of a guaranteed benefit suppresses the signal that they are under-saved and over-promised.

From a systems perspective, the deeper problem is centralization of responsibility. When retirement security is concentrated in a single national scheme, the system creates one giant target for political manipulation, mismanagement, or corruption. There is only one set of assumptions to get wrong, one set of levers to pull, one balance sheet for the entire society to lean on. Friction and entropy never really “reset” from the flow of new information because the same monolithic structure carries forward decade after decade. Volatility that should have been expressed as many small, localized failures—bad security selection, overly aggressive withdrawal rates, or under-saving at the household level—is converted into the risk of one massive failure.

A more antifragile approach is decentralization: forcing the retirement contribution stream into thousands or millions of individual accounts rather than one national pot. Australia’s superannuation system is an example that moves in this direction. Employers are required to contribute a fixed percentage of wages—now 12%—into individual superannuation funds owned by workers, on top of their regular pay. Those assets are invested in diversified portfolios and legally ring-fenced for retirement. In a model like this, taking the 12.4% of U.S. payroll that currently feeds Social Security and directing it instead into compulsory individual retirement accounts would transform the system’s dynamics. Rather than one centralized promise, you’d have millions of small, transparent balance sheets. Each new account, each person’s choice of what to invest in, is new information entering the system; each account that is exhausted or closed is a pruning of old information—many small fires instead of one existential blaze.

Decentralization does not eliminate risk. Some people will still under-save. Others will choose poor investments or overestimate how long their nest egg will last. But those are distributed, observable errors. They generate localized volatility rather than a single binary outcome in which an entire national pension promise either holds or fails. The system can learn and adapt: product design improves, default investment options get smarter, and financial education can be aimed precisely where the data show shortfalls. Volatility is allowed to surface early and often, which is exactly what an antifragile system needs.

In France, the challenges facing pension systems take a different form. The French government recently decided to raise the retirement age from 62 to 64, a move prompted by demographic shifts such as increased life expectancies. While this policy shift aims to preserve the solvency of the pension system, it imposes an additional burden on the workforce (increasing friction by lowering work-to-pay ratios). French workers now find themselves contributing for an extended period before they can claim pension benefits, a change that has ignited significant public debate.

National, local, and company pension funds—originally designed as retirement safety nets—have thus inadvertently disrupted the flow of crucial economic information. They create friction in the economy and dull public awareness of the need for personal financial planning and investment for retirement. The delay in conveying this vital information has profound consequences: a large segment of the population remains uninformed and unprepared for retirement, jeopardizing their financial security precisely when pension systems are at their most vulnerable. On top of this lack of information, there is a further increase in friction and entropy when governments and cities are forced to cut productive spending and increase taxes to cover the payouts of these pension plans. Chicago today is a preview of what many systems will look like as they hit the wall: spiraling contributions, shrinking services, mounting anger, and a growing flight from the formal tax base.

Note: While there is much debate about the haphazard and potentially corrupt management of pensions across the world and throughout history, consider this analogy: if every user consistently encountered problems with a piece of software, we typically blame the software for poor design rather than blaming the users. So why don’t we apply the same logic to systems like pension funds? If these systems are consistently mismanaged or fail to meet their objectives, perhaps the flaw lies within the system itself.

In essence, centralized pension systems do not simply add friction, they risk a system-wide ignition point. When individuals mis-save or mis-invest, those are painful but informative small fires: their failures add data to the market, teach future behavior, and remain bounded in scope. But when a centralized entity like Social Security or a national pension scheme fails, it does not simply introduce more volatility—it behaves like a supercharged wildfire that burns through the topsoil of the entire economy. The damage is not confined to one household or one firm; it can strip a country of fiscal credibility, destroy trust in institutions, and leave a scorched landscape that may take generations to repair. If we insist on concentrating retirement risk in a single structure, we should not be surprised when the inevitable correction looks less like healthy volatility and more like an inferno.

The Solution

As I hope the reader can surmise, the fight against volatility, friction, and entropy is not one that we can win. If we are to create systems that do not repeatedly end in collapse and mass suffrage we must embrace these fundamental factors. But how?

Antifragility

In Antifragile, Nassim Taleb highlights a critical concept that humanity has largely overlooked: the opposite of fragility. While we understand resilience and robustness as the ability to withstand damage without breaking, these terms fall short of describing systems or entities that benefit from stress and adversity. Taleb introduces the term “antifragility” to capture this idea: that something which is antifragile not only survives shocks or volatility but actively benefits and thrives in the face of them.

Wind extinguishes a candle and energizes a fire. Likewise with randomness, uncertainty, chaos; you want to use them, not hide from them. You want to be the fire and wish for the wind.

Nassim Taleb, Antifragile

Antifragility is a concept easiest to grasp when using the human body. Lifting weights is actively damaging your muscles: microscopic tears, stress on joints, spikes in heart rate. In the moment, this is painful and destructive. But given rest and nutrition, the body responds by rebuilding the muscle stronger than before. The stressor is not just something to “tolerate”—it is the input the system needs to improve.

Antifragility also exists in economic and social systems. A single restaurant is fragile: one bad season or new competitor and it can disappear. But the local restaurant ecosystem—all the tiny, independent places battling for customers—is antifragile. As some restaurants fail, others learn what works, copy good ideas, differentiate, or innovate to survive. Over time, the quality and diversity of the restaurant scene improves precisely because individual restaurants are allowed to die. Economists often describe this process as a form of “creative destruction,” where new ideas replace weaker ones and the overall system gains from the turnover.

Now imagine a well-meaning city that decides to “save jobs” and minimize volatility by propping up a failing restaurant with subsidies, special tax breaks, or cheap loans. At first, this looks compassionate: a business is “saved,” workers keep their paychecks, and the short-term volatility of a closure is avoided. But the cost is hidden. Local taxes must rise or other public services must be cut to fund the support. But more importantly, the market never receives the signal that this restaurant’s concept, menu, pricing, or management is failing, so no one learns from it. Over time, more weak restaurants line up for help, and the city finds itself quietly supporting an entire ecosystem of mediocrity. Eventually, the burden becomes unsustainable: the city can no longer afford the subsidies, the propped-up restaurants are still fundamentally uncompetitive, and customers start going out less altogether. What began as an attempt to “save” one restaurant evolves into a scenario where the whole local restaurant market risks collapsing at once, not just from fiscal strain, but from the erosion of quality and trust.

Antifragile systems, then, share a basic pattern:

- They are made of many small, fragile parts (cells, firms, restaurants, funds).

- Those parts are allowed to fail and fail quickly and transparently.

- The system uses those failures as information, reallocating resources away from what doesn’t work toward what does.

Individual fragility is inseparable from ensemble antifragility… it is the death of the individual components which contributes to the growth of the ensemble.

Fragile systems do the opposite: they push volatility into the future, dull the signal of failure, and then experience one massive break instead of thousands of small bruises.

Universal Darwinism: Evolution Beyond Biology

Antifragility tells us how systems can benefit from stress. Universal Darwinism tells us why selection is so powerful in the first place.

Richard Dawkins’ mimetics proposed that cultural phenomena such as words, accents, and ideas spread from brain to brain through some process of replication or imitation. Universal Darwinism is the evolution, or the natural selection, that occurs within this process of replication. And when we realize that everything we do, say, or make all starts as an idea. Then we can apply Darwinian principles Universally.

Philosopher Daniel Dennett calls Darwin’s idea a kind of “universal acid”: once you really accept that complex design can emerge from a blind, bottom-up selection algorithm, it eats through almost every traditional concept and leaves a transformed landscape behind. If selection can build an eye or a rainforest, it can also shape markets, technologies, and institutions. The same logic that pruned unfit organisms over billions of years is constantly pruning unfit business plans, governance structures, and social norms.

Even our perceptions appear to be tuned by this process. Donald Hoffman’s “Case Against Reality” argues that evolution selects not for organisms that see the world “as it really is,” but for organisms whose perceptions are good at tracking payoffs. In other words: nature doesn’t reward truth; it rewards effectiveness.

Now zoom back out to societies. In a healthy market, every restaurant, startup, and policy proposal is a hypothesis being tested against reality. Entrepreneurs launch ideas into the environment: pricing models, new technology, kitchen layouts, hiring strategies. Customers, workers, and investors provide the selection pressure. When a restaurant fails, the owner suffers, and that is real human pain, but the information encoded in that failure is priceless. It tells the neighborhood what doesn’t work at that price, in that location, with that concept. Competitors adjust. New entrants try something different. The “idea ecosystem” gets sharper, fitter, more aligned with what people actually value.

That’s Universal Darwinism at work: ideas, not just organisms, undergoing relentless trial-and-error against a hard environment. The ensemble (the restaurant scene, the city’s economy, the culture of entrepreneurship) can become antifragile precisely because individual ideas and ventures are allowed to die. Their failure is not just a loss; it is a signal, a small fire that clears out underbrush and makes room for better designs.

But when we try to smooth volatility from above, we interrupt this selection process. We take the risk or fragility from individuals and transfer it to the entire ecosystem itself. What could have been a series of small, informative fires becomes a delayed and supercharged fire that scorches the topsoil.

Creating an Antifragile Society

So, what would it mean to design institutions that work with antifragility and universal Darwinism instead of against them? At a high level, it means accepting three hard truths:

So, what would it mean to design institutions that work with antifragility and universal Darwinism instead of against them? It begins with accepting that friction and entropy are not policy choices but universal laws. The second law of thermodynamics tells us that, in an isolated system, entropy can only stay the same or increase over time, never decrease. Every attempt to legislate, subsidize, or centrally manage them away is ultimately an illusion. When governments suppress volatility with guarantees, bailouts, and “safety nets” that promise to erase downside, they don’t delete entropy—they re-route it. The individual may feel temporarily protected, but the system absorbs the risk and becomes brittle. And when a brittle system finally breaks the individual who was “protected” loses everything alongside it.

The antidote is to design societies less like a single overprotected organism and more like humanity as a whole. Individual humans are fragile; we age, we get sick, and we die. But the human species is astonishingly resilient because new humans are constantly being born, old ones pass away, and natural selection continually prunes and recombines traits over generations. Darwinian evolution, as Dennett’s “universal acid” metaphor suggests, is a selection engine that, given enough variation and time, can produce systems that endure on cosmic timescales. A single person cannot outlast entropy, but a self-renewing population can persist for millions of years; in principle, a well-designed, continuously renewing civilization could last as long as stars and black holes themselves.

If friction and entropy are universal, then truthful information is the closest thing we have to a counterweight. In information theory, information is literally defined as the reduction of uncertainty; entropy is the formal measure of that uncertainty or disorder. When we increase reliable signal—when prices, balance sheets, and economic data reflect reality instead of political convenience—we don’t magically halt entropy, but we do stop it from compounding unseen. Systems become more predictable and adaptable. Markets work on this principle: the more real information is embedded in prices, the more those prices serve as compressed, usable summaries of the world. In that environment, volatility is not pure chaos, but a process of truth-discovery—prices adjusting to new information.

Designing an antifragile society, then, means letting truth and selection do their work. It means allowing new people, new firms, and new ideas to enter, and letting outdated institutions, bad policies, and failed experiments exit, instead of preserving everything indefinitely. Each birth, each experiment, each honest failure is information added to the system. Each hidden loss, each guaranteed rescue, each suppressed correction is information withheld. When we choose the former, we get many small fires that keep the forest alive. When we choose the latter, we build toward a single super-fire that threatens to burn the topsoil of the entire civilization.

In Conclusion

Humans may not live very long, but humanity can endure—if we stop trying to outlaw volatility and instead build systems that feed on it. That means designing institutions that expect failure, ingest it, and grow stronger because of it, the way a healthy forest relies on many small burns to avoid a single, sterilizing inferno.

May we, as individuals and as societies, learn to die, so that the larger “we” may live for millions of years!

I hope, by now, the reader can return to the questions at the beginning of this article and answer them for themselves. And if not, or if you disagree, I’d love to continue the conversation, so feel free reach out!